How To Compare Trauma Insurance Quotes

Ever wondered what would happen if you were unable to work while you recovered from a major illness or injury? Who would take care of your mortgage or bills?

Trauma insurance is designed to pay out a lump sum for you and your family if you suffered a serious illness or injury.

Typically, these will be illnesses such as cancer, heart attacks, strokes, major burns or a condition that puts you in intensive care.

These are common health issues – chances are you may know somebody who has been affected.

It’s where trauma insurance comes into its own: giving you a lump sum so you don’t have to worry about finances while you’re unable to work.

Key Points

Trauma insurance provides you a lump sum to help with your finances if you’re unable to work, as well as covering your medical or rehabilitation costs.

The most common types of illnesses covered by trauma insurance include cancer, heart attack, coronary heart disease and stroke.

Trauma insurance offers more comprehensive cover than income protection.

What is trauma insurance?

Trauma insurance, also known as 'trauma cover' or 'critical illness insurance', is a form of life insurance designed to give you protection if you're diagnosed with a serious illness or suffer an injury.

The purpose of trauma insurance is to provide an immediate lump sum payment which helps you focus on recovery without having to worry about work or money.

Below is a quick way of understanding what living expenses trauma insurance is designed to cover:

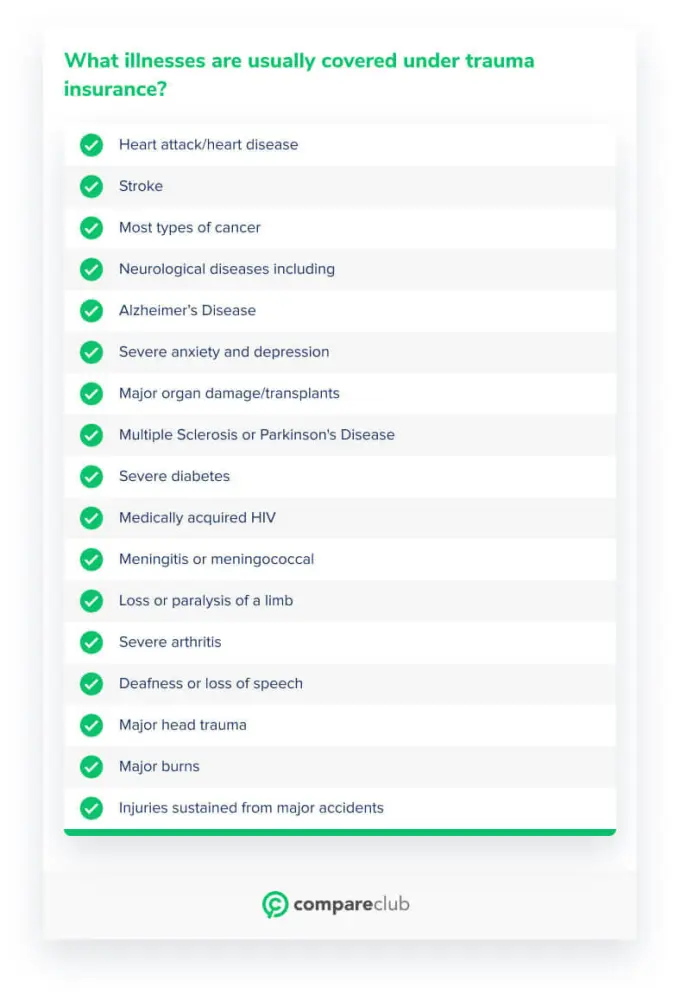

Which conditions are covered under trauma insurance?

Mortgage repayments |

|---|

Living expenses if you're not earning a salary |

Medical and rehabilitation costs |

Ongoing nursing or therapies |

Adapting your home or vehicle to your health needs |

Which conditions are covered under trauma insurance?

Most providers list more than fifty conditions for inclusion in their trauma insurance policies.

While rules and requirements vary among insurers, illnesses which are generally considered traumatic include those listed in the chart below:

What illnesses are sually covered under trauma insurance?

Heart attack/Heart disease |

|---|

Stroke |

Most types of cancer |

Neurological diseases including |

Alzheimer's Disease |

Severe anxiety and depression |

Major organ damage/transplant |

Multiple Sclerosis or Parkinson's Disease |

Severe diabetes |

Medically acquired HIV |

Meningitis or meningococcal |

Loss or paralysis of a limb |

Severe arthritis |

Deafness or loss of speech |

Major head trauma |

Major burns |

Injuries sustained from major accidents |

This list may seem limited but they're also incredibly common.

Heart disease is the leading cause of death in Australia according to the Heart Foundation*, while one in two Australians will get cancer at some point in their lives**.

Cerebrovascular disease - which includes strokes - and Alzheimer's and dementia are also conditions that can severely impact your ability to work.

In essence, while it's not the happiest of thoughts, the conditions which you're likely to suddenly suffer incapacity or die from are included in trauma cover.

That said, it's important to read the Product Disclosure Statement (PDS) when researching policies to understand exactly what's covered and determine whether a provider is right for you.

Compare & SaveWhich illnesses and injuries aren't covered by trauma insurance?

Not all injuries and illnesses are covered by trauma insurance.

Your insurance provider will list the specific conditions they cover in your policy.

Private health insurance can also help with some of the out-of-pocket medical expenses for conditions not included in your trauma insurance.

Does trauma insurance cover COVID-19?

Every policy is different and many insurers are still working out the implications of the coronavirus but trauma insurance won't cover you if you pass away from COVID-19.

However, if the virus results in one of the conditions covered - for example, you're taken into intensive care or suffer any of the conditions listed - then you may be able to make a claim under your trauma insurance.

What's the difference between trauma insurance, income protection and total and permanent disability insurance (TPD)?

It's a good question, and one that can be confusing to a lot of people, so we'll break down the different types of insurance for you.

Trauma insurance is primarily designed to offer a short term cash buffer if you need to take time out for a serious injury or medical condition.

It's awarded as a single payment intended for immediate financial relief.

So if you're worried about paying your mortgage or providing for your family while ill, the lump sum can help relieve any immediate financial stress.

This is different from TPD and income protection insurance, which provides longer term financial cover for many of the same illnesses or injuries but can take longer to pay out.

Income protection provides regular payments up to 70% of your income for a set period of time while you're temporarily unable to work, while TPD provides ongoing payments if your illness or injury means you're permanently unable to work.

It's not uncommon for people to bundle a number of life insurance policies together.

For example, if you're covered for both trauma and income protection, then you may use income protection to cover day-today living expenses while the trauma payout may be used to pay off any gaps in medical expenses or allow your partner to take unpaid leave from work.

If you're bundling policies together, the cost will typically be cheaper than if you take out each policy separately.

Do I need trauma insurance?

Everybody's circumstances are different, but to decide if you need trauma insurance, it's worth asking what would happen if you suddenly lost your ability to earn an income, even for a short period, and looking at the state of your finances.

Take a look at your own personal circumstances, including family history of illness, your dependents and the debts you hold (e.g. mortgage or car loans) to decide how much cover you need.

You will also be asked these questions as part of your application process to help your provider decide whether to cover you and for how much.

Below are some important questions which might help you determine whether trauma cover would support you in the event of a serious illness or injury:

6 questions to work out if trauma cover could help you

if you're worried about your answers, then it could be useul to consider trauma insurance.

1. Could you afford your mortgage payments if your income suddenly stopped? |

|---|

2. What other debts do you have and could afford them without a regular salary? Common debts include: Car loans Business loans |

3. Would your health insurance cover out-of-pocket medical costs for major surgeries or intensive care? |

4. Are you eligible fo government benefits or workers compensation if you were suddenly unable to work? |

5. How much do you have saved? |

6. How financially secure are you right now? |

How much does trauma insurance cost?

Although policies can vary based on a range of aspects, the average premium for a 40-year-old male will be around $86.12 per month (based on $250,000 coverage across Compare Club's panel of insurers).

This cost is slightly cheaper for women.

Here are some factors that may affect your monthly premium:

What affects the cost of trauma insurance?

Everyone's policy cost is different. The following factors will affect your premiums.

Age | Medical History |

|---|---|

Smoking Status | Occupation |

The amount of coverage you need | If you choose a stepped or level premium |

There's two types of ways you can structure your premiums. These are known as stepped and levelled premiums.

Stepped premiums generally begin cheaper but are linked to age and increase each year that you hold your policy.

The younger you are when you take out your trauma cover, the cheaper your initial stepped premium will be, although it may become quite expensive when you get older.

Levelled premiums don't rise with age - although may change if your insurer puts their rates up and will also move with inflation.

They often start out more expensive than a stepped option.

If you plan to hold trauma cover for a substantial period of time it could work out cheaper in the long term.

Both options are viable - it all comes down to your budget, and how long you're expecting to hang onto your cover.

For example, if you only expect to hold your cover for a few years, you may want to consider selecting stepped cover.

Level premiums tend to be more cost effective in the long-term for younger people who expect to hold the cover for a significant period of time.

How do you get trauma insurance?

If you've decided that trauma insurance is right for you, it's worth taking time to compare policies and ensure they're giving you the right level of cover.

You may also want to consider trauma insurance in conjunction with one or more additional forms of life insurance, as they're often complementary, although this depends on your individual circumstance.

This is where Compare Club can help.

We do the heavy lifting by comparing policies from our panel of trusted insurers and presenting you with options that best suit your needs.

There's no obligation to take out a policy and the comparison process is completely free.

If you're ready to get trauma insurance, click below to get started.

Compare & SaveThe information contained in this guide is of general nature only and has been prepared without taking into consideration your objectives, needs and financial situation. As such, it is important that you consider the appropriateness of any advice and the relevant product disclosure statement (PDS) before proceeding. Check with a financial professional before making any decisions.

Heart Foundation, Australian Heart Disease Statistics, August 2020Cancer Council, Cancer Statistics in Australia, August 2020